Global Manufacturing Industry Recovery in 2025 to Follow Sluggish 2024

The global manufacturing economy will remain sluggish in 2024 and is forecast to expand by just 0.6 percent compared with last year. However, it looks set to recover in 2025, the latest data from Interact Analysis reveals. The market intelligence expert explains, except for China, most territories will experience a slight contraction this year, but many will be better off than expected going into 2025.

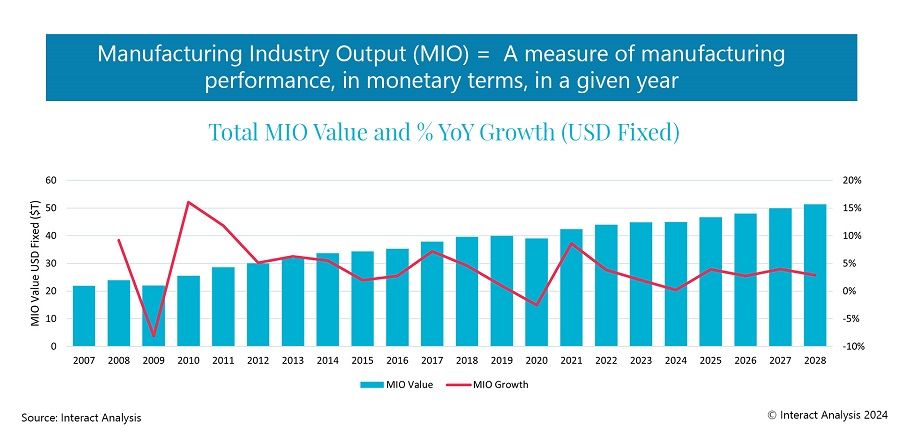

Although Interact Analysis has lowered growth forecasts for 2025 in its latest Manufacturing Industry Output Tracker (MIO), this is the result of a slightly improved global outlook for the end of 2024, which will in turn see most economies finish the year in a stronger position. A slight dip in the growth rate is anticipated in 2026, but manufacturing output is expected to maintain a relatively steady positive trajectory out to 2028.

No clear signs of where recovery will come from

It is still unclear where the global manufacturing recovery will come from and until there is an upturn it is difficult to judge the potential strength. Despite optimistic signs for other territories, the latest MIO includes a slight downward revision for China compared with the previous edition; from 2.8 to 2.4 percent. China as ‘the factory of the world’ is responsible for almost half of the total manufacturing market value and any further reductions in the country’s forecast could well lead to a small contraction in the global MIO figure for 2024.

Consumer resilience coupled with inflation and interest rates slowly starting to fall is pushing up spending worldwide and the US manufacturing economy is strengthening. The semiconductor industry has bounced back from a low point in 2023, boosting outlook for parts of South-Asia heavily reliant on the market sector, including Taiwan, Singapore and South Korea. Dwindling order books and the impact of the higher cost of living have constrained global demand, but there are signs of recovery in consumer spending and post-Covid supply chain problems have eased considerably.

However, there are various economic indicators pointing to a more challenging environment for manufacturers. All four major European manufacturing economies are in a downward cycle, and sentiment for the year remains gloomy. Positive signals from the US may well start to manifest in other regions later in the year, but this has yet to be seen.

Power Transmission Engineering is THE magazine of mechanical components. PTE is written for engineers and maintenance pros who specify, purchase and use gears, gear drives, bearings, motors, couplings, clutches, lubrication, seals and all other types of mechanical power transmission and motion control components.

Power Transmission Engineering is THE magazine of mechanical components. PTE is written for engineers and maintenance pros who specify, purchase and use gears, gear drives, bearings, motors, couplings, clutches, lubrication, seals and all other types of mechanical power transmission and motion control components.