We use cookies to provide you with a better experience. By continuing to browse the site you are agreeing to our use of cookies in accordance with our Privacy Policy.

I don’t know about you, but the recession of 2008-2010 sticks in my mind like a bad penny. Since that time, I am never able to simply say that this year, or next year, is looking good without including the obligatory …”for now”. In the back of my mind, I’m always wondering when the next downturn is going to occur. The 2008 crash happened so quickly, in the midst of a seemingly great economy, I can’t help but worry that I don’t know what I don’t know.

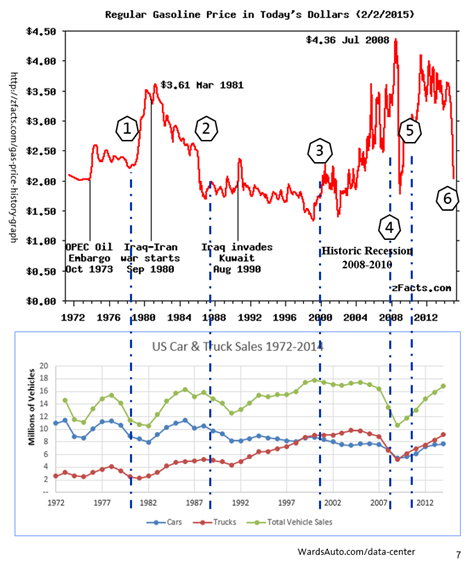

I decided to try and make some sense of it all and see if I could find any patterns with my particular industry. One thing that we all remember from the 2008-10 years is that oil prices went from record highs to record lows so quickly that nobody knew what was going on. Most of us clearly remember this as the cost to fill up our car was outpacing the price of the car. When gas hit $4.00 a gallon, it felt like we were in the beginning of Armageddon. Even the analysts were at a loss for words. Looking at financial headlines these days doesn’t do much good. One article says the next collapse is going to happen this weekend and another says things have never looked better (what’s new?).

Recalling how striking the oil/gas prices fluctuated, I plotted about 40 years’ worth of gas prices against vehicle and vehicle type sales. Half-ton pickup truck sales present an interesting look into the economy because there is no other platform of vehicle that has as many transient buyers; meaning that most of these buyers have the ability to downsize when they need to. Unlike people that actually work for a living, us concrete cowboys don’t have to have a truck. If people feel good about the economy, we sell more trucks and vice versa.

If we use cost of fuel as an indirect measure of vehicle sales, we clearly see that when fuel prices stay low, non-commercial truck sales increase. If we can draw some basic conclusions from the charts on the right:

Continued high fuel prices leave the truck market primarily to functional users.

As fuel prices drop, truck sales increase, suggesting more people using trucks as a flexible vehicles, though car sales remain strong. People aren’t trading their cars for trucks yet.

After 15 years of stable / low fuel prices, truck sales surpass car sales for the first time ever.

As fuel prices continue to increase for 2 years, truck sales begin to drop before total vehicle sales drop heading into a recession.

Total vehicle sales climb with pent-up demand, though with high fuel prices, truck sales do not outpace car sales as uncertainty in the market remains.

Oil price crash of 2014-15 mostly blamed on over-production coupled with softened global demand. US fracking has been a key added source in overproduction as domestic inventory is at an all-time high. Trucks sales again begin to outpace car sales.

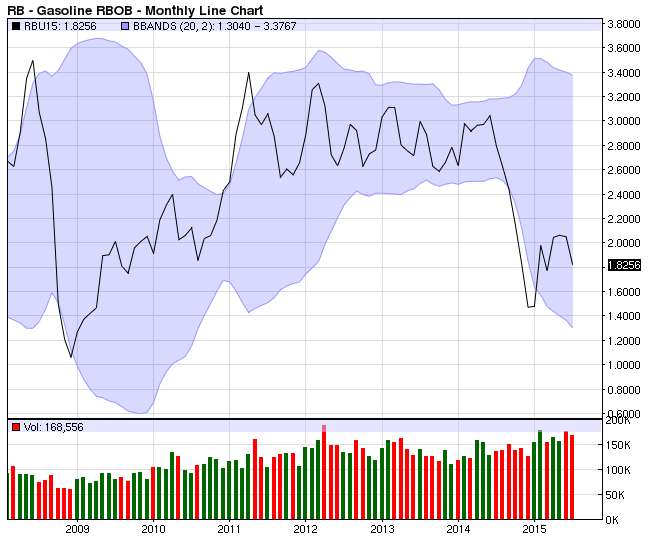

Something that gives me a little comfort is that oil and gas prices are appearing relatively stable. There have been a couple of little blips over the last few years, but overall, prices haven’t been too high or too low. Speculators believe that the Iran nuclear deal could stabilize that region, providing even more stability (so we hope). If you add US fracking into the mix, we now have ample capacity and are no longer shaken by one or two oil countries going into conflict.

So if you wanted my $.02 on the medium term outlook for the economy. It appears things are looking pretty good…for now.